Get ready for California’s climate laws: SB 253 and SB 261

September 28, 2024

On October 7, 2023, California Governor Gavin Newsom officially signed the Climate Corporate Data Accountability Act (SB 253) and the Climate-Related Financial Risk Act Senate Bill (SB 261) into law—as part of the Climate Accountability Package. On September 27, 2024, Governor Newsom signed SB 219 into law, introducing amendments to streamline the implementation of SB 253 and SB 261.

These bills are an important step towards helping California reduce its greenhouse gas emissions and achieve its ambitious zero-carbon goals. More than 10,000 companies are expected to begin their first disclosures in 2026.

This article provides an overview of what businesses need to know to prepare for these regulations, covering the scope, affected entities, reporting timelines, disclosure requirements, and comparisons to the SEC’s climate-related disclosure rules.

SB 253, known as the Climate Corporate Data Accountability Act, requires public and private companies companies operating in California with annual revenues over $1 billion to disclose their Scope 1, 2, and 3 greenhouse gas (GHG) emissions in alignment with the GHG Protocol. The bill is estimated to impact 5,000+ companies. Annual reporting will begin in 2026, with Scope 3 emissions and phased-in assurance levels starting in 2027.

This bill allows regulators, investors, and the public to more effectively assess corporate environmental performance, setting a national and global trend for climate data transparency.

What is SB 261?

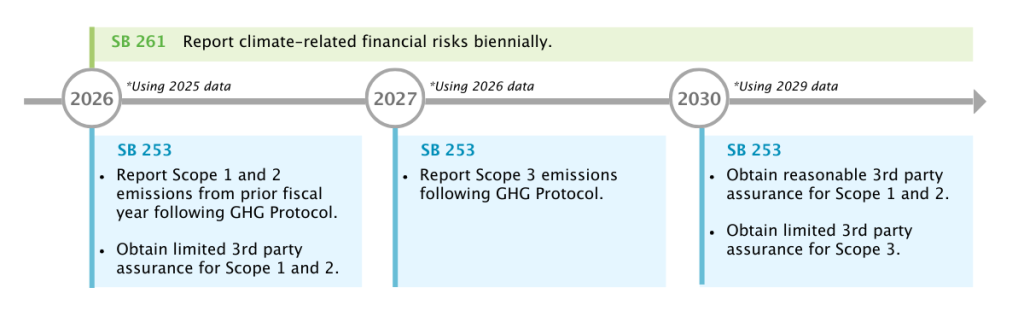

SB 261, known as the Climate-Related Financial Risk Act, mandates that public and private companies operating in California with annual revenues exceeding $500 million report on climate-related financial risks and the measures they have adopted to mitigate or adapt to those risks. Aligned with the Task Force on Climate-related Financial Disclosures (TCFD) framework, it is expected to impact 10,000+ companies, including U.S. subsidiaries and non-U.S. companies meeting the criteria. Companies must begin biennial reporting by January 1, 2026, with subsequent reports due every two years.

SB 261 integrates climate risks into corporate financial reporting, encouraging long-term strategies that could potentially redirect investments toward more sustainable businesses.

What is SB 219?

SB 219, titled “Greenhouse gases: climate corporate accountability: climate-related financial risk,” introduces several amendments to SB 253 and SB 261 to streamline reporting while maintaining transparency. Notable changes include:

Extended CARB implementation deadline: The California Air Resources Board (CARB) has six additional months, extending from January 1 to July 1, 2025, to develop and adopt implementing regulations for emissions reporting. The reporting timelines for companies remain unchanged.

Scope 3 disclosure timing: Instead of requiring Scope 3 emissions to be disclosed within 180 days of Scope 1 and 2 emissions, CARB now has discretion in setting the timeline for Scope 3 disclosures, though the general reporting for Scope 3 is still expected to begin in 2027.

Consolidated emissions reporting: Companies can consolidate their GHG emissions reports at the parent company level under SB 253, similar to the provisions in SB 261, simplifying the process for subsidiaries.

Filing fee deadline: The requirement for companies to pay filing fees upon submitting emissions disclosures has been removed, though the annual fee obligation has not been eliminated.

How do SB 253 and SB 261 compare to the SEC Climate Rules?

These state bills align with a broader global movement toward transparent climate-related data reporting, including the U.S. SEC’s climate-related disclosure rules.

Scope: The SEC rules apply to all publicly traded U.S. companies—an estimated 7,000 entities. In contrast, SB 253 will affect more than 5,000 companies and SB 261 will impact over 10,000 companies, including both public and private entities, based on revenue thresholds.

Reporting framework: The SEC rules are based on a combination of the TCFD framework (similar to SB 261) and the GHG Protocol (similar to SB 253). However, the SEC allows more flexibility in calculation methods, while SB 253 mandates that companies strictly follow the GHG Protocol’s calculation standards.

Scope 3 reporting: Disclosure of Scope 3 emissions is NOT required under the SEC’s final rules, although it was initially proposed. In contrast, SB 253 mandates companies to report Scope 3 emissions starting in 2027.

When should companies report?

Under SB 253, corporations within scope will need to begin reporting in 2026 (using 2025 data), with a phased-in approach for indirect emissions (Scope 3) and mandated assurance levels.

Starting 2026: Report Scope 1 and 2 emissions from the prior fiscal year following GHG Protocol using 2025 data and obtain limited 3rd party assurance for Scope 1 and 2.

Starting 2027: Report Scope 3 emissions following GHG Protocol using 2026 data. (The exact timing will be determined by the CARB.)

Starting 2030: Obtain reasonable 3rd party assurance for Scope 1 and 2 using 2029 data.

Under SB 261, all corporations within scope will need to report on climate-related financial risk and make this report available to the public on or before January 1, 2026, using data from 2025.

SB 253 and SB 261 disclosure requirements

SB 253 requirements

Corporations are required to provide standardized annual climate data reports that meet the following requirements:

In-line with the GHG Protocol: Companies will need to measure and report Scope 1, 2, and 3 emissions in accordance with the Greenhouse Gas Protocol standards, following the Scope 3 calculations that detail acceptable primary and secondary data sources such as the use of industry averages, proxy data, and other generic data for Scope 3 emissions calculations.

Public availability: Public disclosures must be easily accessed and understandable for consumers, investors, and other stakeholders and should include detailed GHG emissions data across Scope 1, 2, and 3 emissions. Disclosures will be published/available on the digital platform developed by the state board’s contracted emissions reporting organization.

Consolidation: Emissions reports can be consolidated at the parent company level, and subsidiaries with a qualifying parent company do not need to report separately. (Introduced by SB 219.)

Assurance: Starting in the first year of disclosure, assurance on emissions will be required, with a phased-in approach for reasonable third-party assurance for Scope 1 and 2 and limited assurance on Scope 3 in 2030.

Penalties: Administrative penalties for non-filing, late filing, or failure to meet requirements in other regards will be regulated and authorized by the state board. These penalties will not exceed $500,000 per reporting year.

SB 261 requirements

Covered entities must biennially prepare a climate-related financial risk report that meets these requirements:

In-line with the TCFD: Companies must follow the framework and disclosures of the Final Report of Recommendations of the Task Force on Climate-related Financial Disclosures (June 2017) from TCFD, or another equivalent reporting requirement (e.g., International Sustainability Standards Board—ISSB—Standards).

Disclose climate risk mitigation efforts: Reporting entities must disclose the measures you plan to take to reduce and adapt to your reported climate-related financial risk.

Disclose missing data: Provide a detailed explanation of any reporting gaps and your strategy to complete future disclosures.

Public availability: Corporations will need to biennially publish their reports on their own website.

Consolidation: Risk reports can be consolidated at the parent company level, and subsidiaries with a qualifying parent company do not need to report separately.

Assurance: A climate reporting organization will be contracted to identify inadequate or insufficient reports. If identified, the administrative penalty may be up to $50,000.

Future assessments by the CARB

It should be noted that under SB 253, the California Air Resources Board (CARB) is also committed to future assessments of deadlines and assurance provider qualifications, the development of a digital platform, and a large-scale report:

Deadlines and assurance: On or before January 1, 2030, the state board will review and update, as needed:

Public disclosure deadlines to ensure companies can submit Scope 3 emissions disclosures on time.

The qualifications for third-party assurance providers are “based on an evaluation of trends in education relating to the emission of greenhouse gases and the qualifications of third-party assurance providers.”

Reporting standards: Starting in 2033 and every five years thereafter, the state board will assess current GHG accounting and reporting standards. If deemed appropriate, it may develop and adopt new regulations accordingly.

Digital platform: Although a date has not been determined, the state board committed to developing a digital platform/reporting program by contracting with an emissions reporting organization that will receive and make publicly available corporate disclosures. This platform is intended to provide companies’ aggregated data in various ways and cross-linearly in an electronic format for public access and use.

Public report: On or before July 1, 2027, the state board will also contract with an academic institution or lab to prepare a report of the submitted public disclosures, which will likewise be made publicly available on the digital platform.

California Assembly Bill 1305: Voluntary carbon market disclosures

This bill receives less attention but was likewise approved by the governor on Oct. 7, 2023. It mandates that businesses marketing or selling voluntary carbon offsets (VCOs) in California must disclose comprehensive information about completed, uncompleted, and unsuccessful VCOs on their websites. Details about the carbon offset project(s) must include the protocol used, project location/timeline, emission reduction specifics, third-party validation, and more, which are also mandated from companies using offsets to claim carbon neutrality or net-zero emissions. Information needs to be updated annually, and non-compliant businesses will face civil penalties. The timeline for implementation has not been released.

How can Aligned Incentives help you get ready?

Aligned Incentives provides a science-based sustainability platform that helps global organizations effectively measure, report, and mitigate environmental impacts and climate-related financial risks while ensuring compliance with SB 253 and SB 261.

Efficient Scope 3 Reporting: Collecting primary data for Scope 3 emissions from global suppliers can be challenging and potentially less accurate than secondary sources. Our AITrack platform can help you comply with SB 253 Scope 3 requirements by efficiently integrating primary and secondary data in line with the GHG Protocol. Grounded in process-based life cycle assessments that cover over 300,000 Scope 3 activities, our solution provides accurate, granular footprint estimates of your value chain emissions and minimizes reliance on primary supplier data.

TCFD Risk Assessment: Aligned Incentives’ TCFD module enables you to seamlessly leverage your footprint and combine it with a variety of Intergovernmental Panel on Climate Change (IPCC) and International Energy Agency (IEA) scenarios to assess your transition/financial and physical risks. We do so following TCFD guidance, enabling you to meet SB 261 requirements.

Transparency and Assurance: The robustness of AITrack and our accounting system ensures auditability, traceability, and security. It offers detailed documentation down to the line-item level, simplifying the auditing and assurance processes and setting you up for success.